Extending credit is a standard business practice — but without a structured process for evaluating customer creditworthiness, small businesses expose themselves to late payments, defaults, and cash flow disruptions.

Outstanding invoices from customers who don't pay on time drain the working capital your business needs to operate, invest, and grow.

Without documented credit agreements, you have limited legal options when a customer defaults — leaving you with little more than a bad debt write-off.

Without a business credit check, you cannot identify customers who have already defaulted elsewhere or who carry active liens and judgments against them.

Bankruptcies, lawsuits, and court judgments are visible in credit reports — but only if you look. Skipping the check means missing critical red flags before it's too late.

Granting credit to customers already overextended with other vendors multiplies your exposure — and your likelihood of joining a long list of creditors chasing the same unpaid balances.

A single large defaulted account can destabilize cash flow and force difficult decisions about payroll, inventory, or operations — risks that a credit check could have prevented.

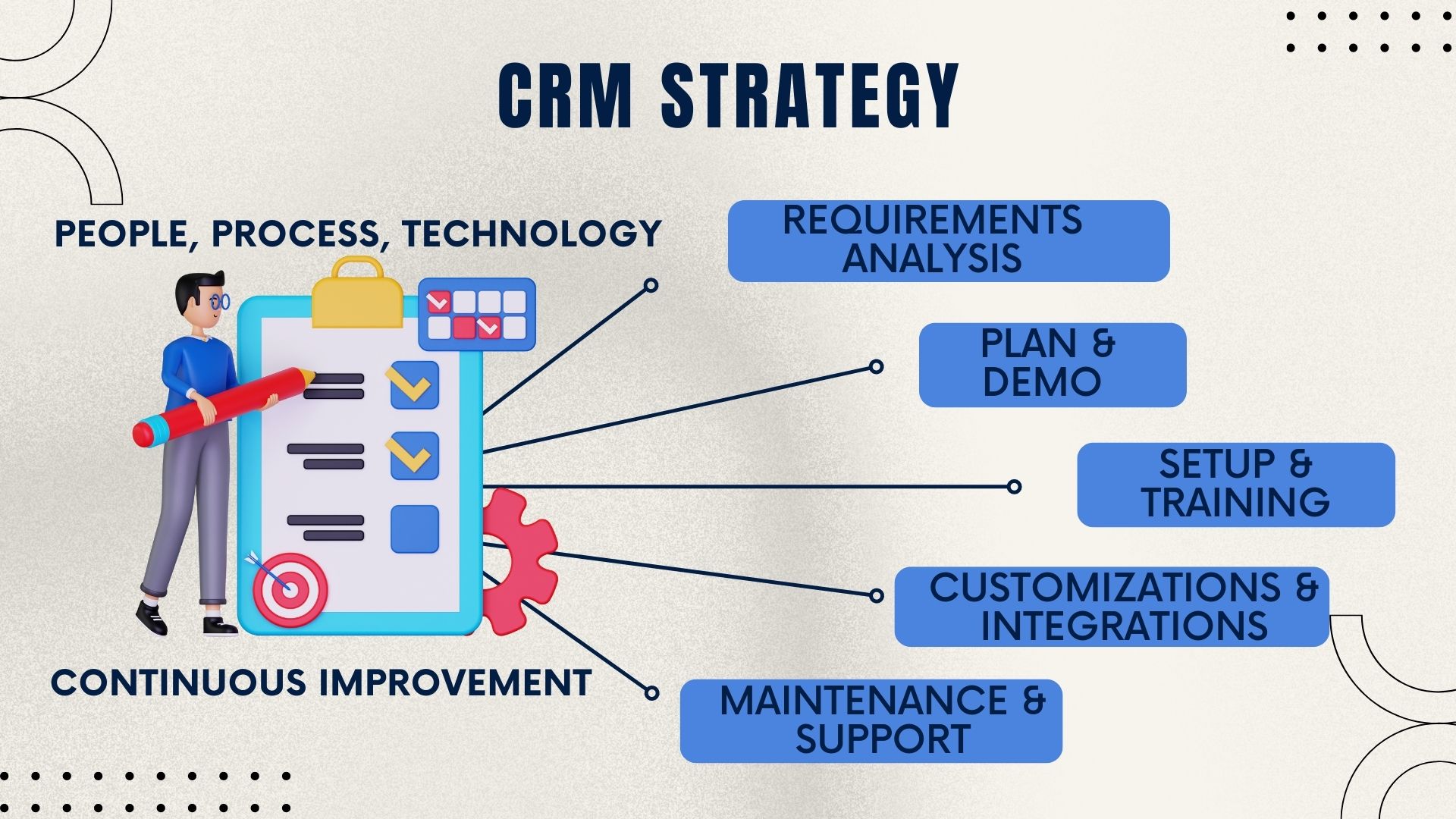

A disciplined business credit check draws on multiple sources — from references and reports to financial statements and letters of credit. Here is how to use each one effectively.

Performing a one-time business credit check is only the beginning. Salesboom CRM gives you the tools to monitor, track, and manage every credit relationship on an ongoing basis.

Salesboom brings over 22 years of CRM innovation to help small and mid-sized businesses manage financial risk with confidence — from the first credit check to ongoing relationship monitoring.

Build your own credit risk tabs, flags, and fields without custom development — designed to adapt to any industry or credit workflow you require.

Every payment interaction, note, and credit decision is stored in a single customer record — ensuring nothing falls through the cracks, regardless of team size.

Set rules to automatically flag at-risk customers, trigger follow-up tasks, or escalate overdue accounts based on your specific criteria and risk thresholds.

Native QuickBooks and Outlook integration connects your credit data with your accounting and communications workflows — eliminating silos and manual reconciliation.

No hidden fees, no vendor lock-in, and predictable monthly pricing starting at $14/user — accessible for businesses of any size, from startups to growing enterprises.

Trusted by 3,500+ businesses across 159 countries to manage customer relationships and financial risk — with the track record to back every claim we make.

Good credit management is not just about protecting your business — it is about building trust-based relationships that benefit both parties over the long term.

As a business extending credit, you need the confidence that payment will arrive on time, clear documentation to protect your legal rights, and full visibility into customer behavior before problems escalate.

Customers seeking credit want to be evaluated fairly and given the opportunity to demonstrate their reliability. They want clear terms, transparent expectations, and a process that doesn't feel adversarial.

Both parties fear a difficult credit conversation could harm an otherwise positive business relationship. Over-caution can push good customers away; under-caution creates financial damage.

Whether you are extending credit to 10 customers or 10,000, your process needs to be consistent, auditable, and scalable. Manual spreadsheets and informal approvals work at the start — but they create serious risk as volume increases.

Credit application forms and evaluation criteria that are consistent across every customer — removing subjectivity and enabling fair, auditable decisions.

A single CRM repository for all credit decisions — accessible to authorized team members and searchable across your entire customer base.

Routine follow-ups and payment reminders run automatically — freeing your team to focus on high-priority accounts and exceptions that need human judgment.

The right team members handle the right decisions — with role-based access ensuring that credit approvals follow your organization's authority structure.

Monitor your entire receivables portfolio at a glance — identifying concentration risk, aging trends, and accounts that need immediate attention.

Real-time flags on overdue accounts push directly from your CRM to QuickBooks — keeping your accounting team informed without manual data entry.

Defined escalation paths for high-risk or delinquent accounts ensure that the right manager is engaged at the right time — before accounts become uncollectable.

Salesboom's modular CRM architecture supports all scalability capabilities out of the box — with flexibility to customize for your specific industry and credit model.

Poorly managed credit extensions are one of the most common causes of small business cash flow crises. A structured approach to credit management mitigates these risks before they become serious problems.

Credit reports and financial statements reveal payment history patterns before you commit to terms — identifying customers likely to default before you extend your first invoice.

Letters of credit and documented credit agreements provide enforceable legal recourse if disputes arise — protecting your rights and giving you a clear path to resolution.

Evaluating customer creditworthiness before extending terms prevents overextension that could leave your business short of the operating capital it needs to function.

Clear credit terms set mutual expectations from the start — reducing misunderstandings that damage long-term partnerships and protecting both parties' interests.

A repeatable credit evaluation process allows your business to grow its customer base confidently — without taking on disproportionate financial exposure as volume increases.

Ongoing CRM monitoring ensures that changes in a customer's payment behavior surface early — giving you time to adjust terms or escalate before the situation deteriorates.

Get clear, practical answers to the most common questions about business credit checks, credit reports, financial analysis, and CRM-based credit management.

Explore Salesboom's resource library — from CRM product tours to small business finance guides — to help you protect cash flow and grow with confidence.

Explore our comprehensive resource library for small business owners covering finance, operations, and growth. Access it at the Small Business Advice Guide.

Find the right Salesboom plan for your team size and credit management needs. Compare features and pricing at the Edition Comparison page.

Discover how Salesboom CRM is tailored for your specific industry's credit and financial risk requirements. Explore our Industry Solutions overview.

Stay current with the latest Salesboom updates including new credit workflow and automation capabilities. Browse New Features now.

Explore the full suite of Salesboom CRM tools built for small and mid-size business financial management. View our Salesboom Products page.

Access in-depth research and best practices on credit management and CRM strategy for small businesses. Download from our Whitepapers Library.

Get answers fast with our comprehensive knowledge base and customer support resources. Visit the Salesboom Support Center anytime.

Review our uptime and service guarantees — the commitments Salesboom makes to every customer. Read our CRM Service Level Agreement.

Salesboom's customizable CRM helps small businesses track credit risk, automate payment follow-ups, and protect their bottom line. Book a free demo and see how easy smarter credit management can be.

Questions? Call: 1-855-229-2043

Discover powerful CRM editions to scale your business efficiently.

A complete CRM suite with Marketing Automation, ERP integration, and Support tools — built for performance and value.

Explore ProfessionalFor large enterprises — automate workflows, unify data, and leverage analytics to drive strategic growth.

View EnterprisePerfect for small teams starting with CRM — manage leads, track sales, and boost productivity with simplicity.

Discover Team